The Goods and Services Tax (GST) that is charged by both the Central and the State government is an all-round tax that is charged on the supply of goods and services. This Goods and Services Tax (GST) is divided into various categories, Integrated Goods and Service Tax (IGST), Central Goods and Services Tax (CGST), and State Goods and Services Tax (SGST) depending on the supply and consumption of goods and services.

As stated above, Goods and Services Tax (GST) is an all-around tax, meaning that it is charged on the goods and services at every level. The tax is not collected from the moment the goods are produced, because they are destination-based. The tax is collected from the last point, where the consumption takes place. This is why Goods and Services Tax (GST) is divided into CGST, SGST, and IGST, depending on where and how it is being collected.

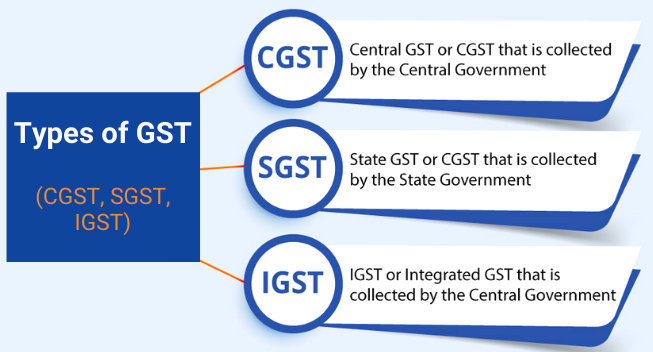

Types of Goods and Services Tax (GST)

Both the Central and State government needs finances to carry out the various agendas assigned to them for the welfare of the country. To secure those finances, the government charges taxes on various goods and services that are bought, imported, or exported in or by the country.

The citizens of a country must pay the taxes levied on the goods and services by the government. Taxes are levied on various goods that are bought by the citizens like, food, luxurious items, electronics, furniture, et cetera. With these taxes, the government works on improving the condition or developing the roads, railways, medical facilities, academic institutions, public offices, et cetera.

Central Goods and Services Tax (CGST)

CGST or Central Goods and Services Tax is levied by the government on the movement of goods and services within one state and the rates of the GST remain the same. All the taxes that were earlier applied on the goods and services and indirect tax by the Central government, now come under Central Goods and Services Tax. Central Goods and Services Tax is applicable in every state of India except Jammu and Kashmir.

When goods and services are consumed within a state, then both Central Goods and Services Tax and State Goods and Services Tax is applied. The revenues of the Central Goods and Services Tax are collected in the treasury of the Central government.

Integrated Goods and Services Tax (IGST)

Integrated Goods and Services Tax or IGST is levied by the government on the goods and services that are supplied from one state to another and the rate of GST differs.

Integrated Goods and Services Tax or IGST is applicable on both the import and export of goods and services to and from India. The rate of GST on exports is zero under Integrated Goods and Services Tax or IGST and the taxes are shared by both Central and State government.

State Goods and Services Tax (SGST)

SGST or State Goods and Services Tax is levied by the government on the movement of goods and services within one state and the rates of the GST remain the same. All the taxes that were earlier applied on the goods and services and indirect tax by the State government, now come under State Goods and Services Tax. As stated above, when goods and services are consumed within a state, then both Central Goods and Services Tax and State Goods and Services Tax is applied.

Why is GST divided into GGST, SGST and IGST?

Both the central and the state government has the right when it comes to collecting taxes on goods and services independently. Both the central and the state governments are assigned specific responsibilities. To carry out those responsibilities, finance is required by the central and the state government. That finance comes in the form of taxes levied by the central and the state government on goods and services.

Before the Goods and Services Tax or GST was introduced, the government of the state used to function independently, and many indirect taxes were charged by the state government on the goods and services. When Goods and Services Tax or GST was introduced, it joined all the taxes under one category. Goods and Services Tax or GST was introduced with the sole aim of uniting all the taxes levied in the nation into one.

But the transparency of the tax had to be ensured as the single tax had to be levied on many goods and services on a very large scale. To ensure that there was no hassle in levying the tax on various goods and services, Goods and Services Tax or GST was further split into three more categories of Integrated Goods and Service Tax (IGST), Central Goods and Services Tax (CGST), and State Goods and Services Tax (SGST) depending on the supply and consumption of goods and services. This ensured the transparency of the tax collection and that the state government has enough finances to keep working on the various agendas.

Types of GST Rates Applicable on Product

The rate of taxes to be levied on the goods and services is decided by the GST Council. It meets every year to discuss the matters related to the GST taxes. There is no specific time decided for the annual meet but whenever the GST Council deems it necessary. The GST Council has divided the rates of GST into 6 slabs.

5% GST Rate

The rate of 5% GST is levied on goods that are of basic necessity to everyone. Goods like sugar, oil, spices, fertilizers, cream, yogurt, cheese, cashew nuts, raisins, coffee, coal, fertilizers, tea, ayurvedic medicines, agarbatti, sliced dry mango, cashew nuts, sweets, handmade carpets, lifeboats, fish fillet, unbranded namkeen, and life-saving drugs

12% GST Rate

The rate of 12% is levied on goods like citrus fruits, pickles, murabba, chutney, jam, and jelly. Kinds of ketchup and food dressings are also included in the 12% GST slab along with all the diagnostic kits and reagents. Plastic and paper products like spectacles, books, crockery are levied at a 12% GST rate. 12% rate is also levied on wooden toys and computers, geometry boxes, railway coaches, et cetera. 12% GST rate is also levied majorly on goods that are processed.

18% GST Rate

The rate of 18% GST is levied on the products like oils, toothpaste, tripods, soaps, bindis, chocolates, pens, bags, headgear and their parts, pipes, tire, hooks, and eyes, machinery and accessories, industrial electronics, sportswear, and games, bamboo furniture, et cetera. 9% out of the 18% goes to the Central Goods and Services Tax and the other 9% goes to the State Goods and Services Tax.

28% GST Rate

The rate of 28% GST tax is levied on luxurious items like cigarettes, caffeinated beverages, pan masala, motor cars and motorcycles, air conditioners, refrigerators, et cetera. 14% out of the 28% goes to the Central Goods and Services Tax and the other 14% goes to the State Goods and Services Tax.

3% GST Rate

The rate of 3% GST tax of levied on luxurious items like coins, gold, silver, platinum, imitation jewelry, etc. 1.5% out of the 28% goes to the Central Goods and Services Tax and the other 1.5% goes to the State Goods and Services Tax.

0.25 GST Rate

The rate of 0.25% GST tax is levied on precious stones. 0.125% out of the 28% goes to the Central Goods and Services Tax and the other 0.125 goes to the State Goods and Services Tax.

Difference between CGST, SGST and IGST

It is very important to understand the 3 types of GST as everyone has to pay them somewhere or another. Let’s have a look at the differences among these three.

| CGST | SGST | IGST |

|

|

|

The existing taxes subsumed are:

|

The existing taxes subsumed are:

|

|

|

|

|

Frequently Asked Questions

Q1. What are the different categories of the Goods and Services Tax levied by the government?

Ans. The Goods and Services Tax (GST) that is charged by both the Central and the State government is an all-round tax that is charged on the supply of goods and services. This Goods and Services Tax (GST) is divided into various categories, Integrated Goods and Service Tax (IGST), Central Goods and Services Tax (CGST), and State Goods and Services Tax (SGST) depending on the supply and consumption of goods and services.

Q2. Why is the goods and services tax split into CGST, IGST, and SGST?

Ans. To ensure that there is no hassle in levying the tax on various goods and services, Goods and Services Tax or GST was further split into three more categories of Integrated Goods and Service Tax (IGST), Central Goods and Services Tax (CGST), and State Goods and Services Tax (SGST) depending on the supply and consumption of goods and services. This ensured the transparency of the tax collection and that the state government has enough finances to keep working on the various agendas.

Q3. Why was the Goods and Services Tax introduced?

Ans. Before the Goods and Services Tax or GST was introduced, the government of the state used to function independently, and many indirect taxes were charged by the state government on the goods and services. When Goods and Services Tax or GST was introduced, it joined all the taxes under one category. Goods and Services Tax or GST was introduced with the sole aim of uniting all the taxes levied in the nation into one.