The Employees’ provident fund started with the annunciation of the Employees’ provident funds on 15th November 1951. Later, the Employees provident fund Act, 1952 replaced it. EPF bill was introduced in parliament in 1952 as bill no. 15 to provide provident fund facility to employees of factories and other institutions. Now, the act is known as Employees’ Provident Funds and Miscellaneous Provision Act, 1952 but is not applicable in Jammu and Kashmir.

The Acts and schemes framed are administered by a tripartite board – Central Board of Trustees, Employees’ provident fund which consists of representatives of Government, employers, and employees.

This board also administers a contributory provident fund, pension scheme, and an insurance scheme for the workers of organized sectors in India. It is one of the largest clientele in the world and the largest volume of financial transactions are undertaken by it. The EFPO assists the board with offices at 122 locations pan India. Ministry of Labor and Employment, Government of India controls the EPFO.

Objectives of EPFO

The EPFO has several objectives for the Employees’ welfare. The EPFO objectives are listed below:

- To make sure that one employee owns only one PF account.

- Easy facilitation of the Compliance.

- To ensure that the organization follows the rules and regulations properly.

- To make online service reliable and improve the services.

- The claim settlement should be done in 3 days.

- Voluntary compliance should be promoted and encouraged.

EPFO Schemes

The board operates 3 schemes-

- The Employees’ provident fund scheme 1952 (EPF)

- The Employees’ Pension Scheme 1995 (EPS)

- The Employees’ Deposit Linked Insurance Scheme 1976 (EDLI)

Let’s discuss about these scheme below.

Employees’ Provident Fund Scheme 1952 (EPF)

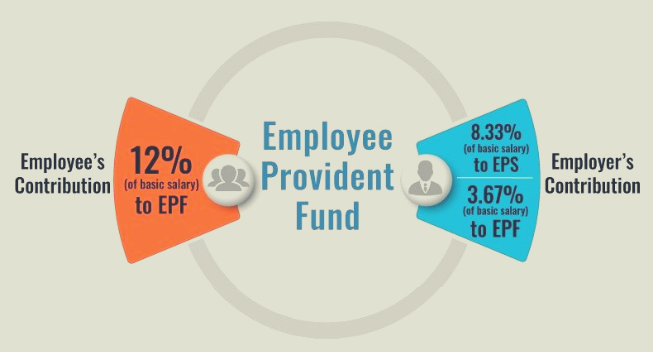

EPF is one of the main schemes operated by EPFO. In this scheme, 12% of the Employees’ basic salary is contributed by both employee and the employer along with dearness allowance toward EPF. The Rate of Interest on EPF is 8.0% p.a.

Details of Employees’ and employer’s contribution toward EPF

Employees’ contribution: 12% of an Employees’ salary is deducted on the monthly basis. The entire amount goes to the EPF account.

Employer’s Contribution: Employers also contribute 12% of the Employees’ salary for the EPF account.

EPF Interest Rate

The current EPF interest rate is 8.50%. The amount is added to the Employees’ and employer’s contribution at the end of the year.

EPF Eligibility

The eligibility criteria for the EPF scheme is:

- The Employees’ income must be less than Rs.15000 per month to register for an EPF account.

- The organization must have more than 20 employees.

- If the organization has less than 20 employees can also join the EPF voluntarily.

- Employees earning more than Rs.15000 can also register for an EPF account with the approval of the Assistant PF commissioner.

- EPF scheme is available in Pan India except for Jammu & Kashmir.

Types of EPF Forms

The table below contains the list of EPF forms and their uses.

| Form Number | Use |

| Form 31 | It is also known as the PF advance form used for obtaining withdrawals, loans, and advances from the EPF account. |

| Form 10D | Used for Availing the monthly pension. |

| Form 10C | Used to withdrawal the fund contributed by the Employer toward EPS. |

| Form 13 | Used to transfer EPF account from the previous job to the current job. |

| Form 19 | Used to claim the EPF account’s final settlement. |

| From 20 | Used to claim the amount by the family member in case of the account holder’s death. |

| Form 51F | Used by the nominee to claim benefits of Employees’ Deposit linked insurance. |

Benefits of EPF Scheme

- EPF allows the saving of money for the long run.

- There is no single lump-sum investment needed. The contribution amount is deducted on a monthly basis which reduced the burden of saving from the employee and also saves a huge amount of money over a long period.

- The employee can easily meet emergency expenses.

- Money can be saved to maintain a stress-free life after retirement.

Employee Pension Scheme 1995 (EPS)

EPS was introduced in 1995 to help employees in the organized sector. The eligibility criteria of EPS and EPF is almost the same.

Under EPS, the employee receives a pension at the age of 58 years old. EPF members can also avail the benefits of this scheme. The employee and employer contribute 12% of the basic salary and the dearness allowance toward EPF. The entire amount of Employees’ contribution is contributed to EPF but 8.33% of the employer’s contribution goes to EPS. It is like a regular income source after retirement.

Eligibility for EPS benefits

- The candidate must be a member of EPFO.

- The age of the candidate must be 58 years.

- In case, candidate defers the pension for 2 years, he will receive the pension at an additional rate of 4% p.a.

- The candidate must have completed 10 years of service.

EPS Contribution

The employer’s contribution is divided into EPF and EPS and Government also contribute in below mentioned ways:

- EPF contribution – 3.67%

- EPS contribution – 8.33%

- Government’s contribution – 1.16%

Employees are not eligible to contribute toward EPS.

EPS Forms

The table below contains the different EPS forms and their uses.

| Forms | Uses |

| Form 10C | It can be used by the beneficiary for the EPF scheme certificate and the withdrawal of pension amount before completing 10 years of service. |

| Life Certificate | It is used by the pensioner to state that he/she is alive and must be submitted to the bank manager where the pension funds are received every November. |

| From 10D | It can be used by members/nominees/widows etc. once the member reaches the age of 50 years. It can also be used for monthly child pension, widow pension, etc. |

| Non Remarriage Certificate | It can be used by Widow/Widower to certify that widower/widow is not remarried and it must be submitted by November on yearly basis. |

| New Form 11 | It can be used by the member to furnish bank and Aadhaar details. After the UAN activation, a cheque must be provided with the name, IFSC code, and account number written on it. |

Benefits of EPS

- EPS is sponsored by the Indian Government, there is no risk to investing in the scheme. The amount that will be returned will be fixed and changes will not be made.

- In case, if widow/widower remarries, the pension will be given to children.

- EPF employees will be automatically enrolled in EPS.

- The minimum amount of pension is Rs.1000.

- In case, widow/widower receiving EPS, they will receive it until their death. And after their death, children will receive until the age of 25 years.

- In case the child is physically challenged, he/she will receive the pension entire life.

Employees Deposit Linked Insurance Scheme

The EDLI is linked to EPS and EPF schemes and the candidates are automatically enrolled in EDLI. The employee cannot choose which scheme he/she wants to join but it can be transferable during the change of jobs.

Contribution to EDLI

- The contribution to the scheme depends on the formula of a fixed percentage of DA and Salary.

- EPF contribution by the employee – 12%

- EPF contribution by Employer – 12% minus EPS contribution

- EPS contribution by Employee- None

- EPS contribution by Employer- 8.33%

- EDLI contribution by Employee- None

- EDLI contribution by Employer – 0.5%

Benefits of EDLI

- Claim amount under the EDLI is 30 times the salary which is calculated as DA+ Basic salary.

- The bonus of Rs.1,50,000 will also be provided at the time of claim.

- The coverage Quantum is directly linked to salary.

- Age and any other individual factor don’t affect an Employees’ eligibility.

- The employer can opt-out of the scheme anytime if the employer has opted for a better scheme for employees.

- The employer can also opt for LIC insurance along with EDLI for the employees.

Documents required for EDLI claim

- Death certificate

- Guardianship certificate

- Succession certificate

- Canceled cheque

Eligibility Criteria for EDLI

Following members are eligible to apply for claiming benefits:

- Nominee under EPF scheme.

- All members of a family, in case of no nomination.

- If there is no nomination and no family, the legal heir can claim.

- Guardian if the minor nominee.

Frequently Asked Questions

Q1. What is the Administrative charged under EDLI?

Ans. For Administrative Charges under EDLI, the employer pays 0.01% amount of the minimum wages.

Q2. What are Assurance benefits under EDLI?

Ans. On the death of a member (in-service), the nominee or any other member will receive the PF benefits along with assured benefits.

Q3. What is PF Toll-Free Number?

Ans. PF Toll-Free number is 1800118005.